Every successful project rests on the backbone of project cost management. In the absence of this discipline, even the most carefully designed projects can falter due to financial pressure. The key to decoding project cost management lies in understanding that it is beyond merely balancing figures on a spreadsheet. You also need to understand how to plan, estimate, track, and manage expenditures.

Research says that nearly 70 percent of projects exceed their initial budgets, often due to inadequate forecasting or limited insight into current expenditures. Read further to learn about the core steps, key processes, and a practical project cost management example that exemplifies a thoughtful project cost management plan.

What is project cost management?

Project cost management as a function includes the planning, distribution, and supervision of a project’s financial resources over its entire duration. Its scope extends well beyond merely cost monitoring. Formulating a comprehensive plan to utilize every dollar or rupee and anticipating possible additional expenses in advance is also part of this domain. It further includes ensuring that expenditures align with the objectives of the project.

Let’s explain it in tactical terms. If you have launched a project, project cost management is what prevents it from exhausting its resources midway. With this discipline, managers can accurately forecast future costs and closely monitor current expenses. They can do all this while making swift adjustments when actual figures differ from initial projections.

When managed correctly, cost control avoids unexpected issues and fosters trust among teams and stakeholders.

Types of project costs

Let’s start by quickly reviewing the various types of expenses that comprise your project budget. Ensure you understand how to categorize them so you can effectively plan and track your progress.

Studies confirm that projects with well-defined cost categorization and clear contingency planning tend to experience fewer overruns. This happens because teams can see where each dollar goes and quickly adjust their spending when conditions change.

Take a closer look at the main types of costs involved in project cost management:

Direct costs

These are expenses that directly contribute to the project deliverables. The bulk of your expenses fall into this bracket, including salaries for your development team, materials, equipment rentals, or contractor fees. You’ll observe that these expenses are easily traceable to specific project activities.

Indirect costs

As the name suggests, these support the project indirectly. Examples include utilities, rent, insurance, and administrative expenses. While you can’t tie them to a single activity, you cannot do without them.

Fixed costs

Fixed costs are expenses that remain constant, regardless of the amount of work completed. To get a better idea, consider examples such as monthly software subscriptions or permanent staff salaries. If you know your fixed costs, you can maintain an account for ongoing commitments even when activity levels fluctuate.

Variable costs

These are just the opposite of fixed costs. Variable costs fluctuate in proportion to the project’s activity level. For instance, costs such as overtime compensation, logistics, and consumables increase in tandem with production. Monitoring these helps avoid financial surprises during the most demanding stages of the project.

Contingency costs

As most project managers are aware, projects rarely proceed exactly as planned. Hence, contingency funds exist. They cover unanticipated hazards, emergencies, or changes that might otherwise compromise schedules or quality.

Understanding why project cost management is important and how it enhances the overall success of your projects is the next step after laying this foundation.

Importance of project cost management

Project managers know that their project success depends on more than simply meeting deadlines. They also need to stay within budget. With prudent project cost management, they can ensure that project spending stays aligned with goals.

Builds financial discipline and predictability

Teams are aware of their spending limits, when to use them, and how to calculate value. According to research, performance and profitability are increased when cost, time, scope, and quality are all managed effectively. Projects function more efficiently and prevent unnecessary waste when cost control is integrated into the process.

Enhances stakeholder confidence

When the budgets are predictable, trust improves. Regular reporting and transparent communication reassure sponsors and clients that funds are being used wisely. Regular stakeholder engagement reduces financial conflict and helps prevent overruns, per a study.

Prevents scope creep

Uncontrolled expansion of scope is one of the biggest threats to a project budget. A clear project cost management plan helps detect these changes early. By tracking deviations against a set baseline, teams can make informed decisions before costs spiral. This keeps both timelines and budgets realistic.

Enables data-driven decision-making

Modern cost management relies on real-time insights, not guesswork. According to RSIS International, projects that utilize real-time tracking and automated reporting achieve measurable savings. When financial data is visible at all times, teams can course-correct quickly and prevent costly surprises.

Strengthens overall project performance

Project cost management fundamentally links scope, quality, and value. It helps teams make better plans, allocate resources wisely, and maintain focus on quantifiable outcomes. Achieving more with the resources you already have is the primary goal of effective cost control. Each team needs a well-defined set of procedures to follow in order for this discipline to be effective in practice.

And to make this discipline work in practice, every team needs a clear set of steps to follow. The next section explores the key project cost management processes that turn strategy into action.

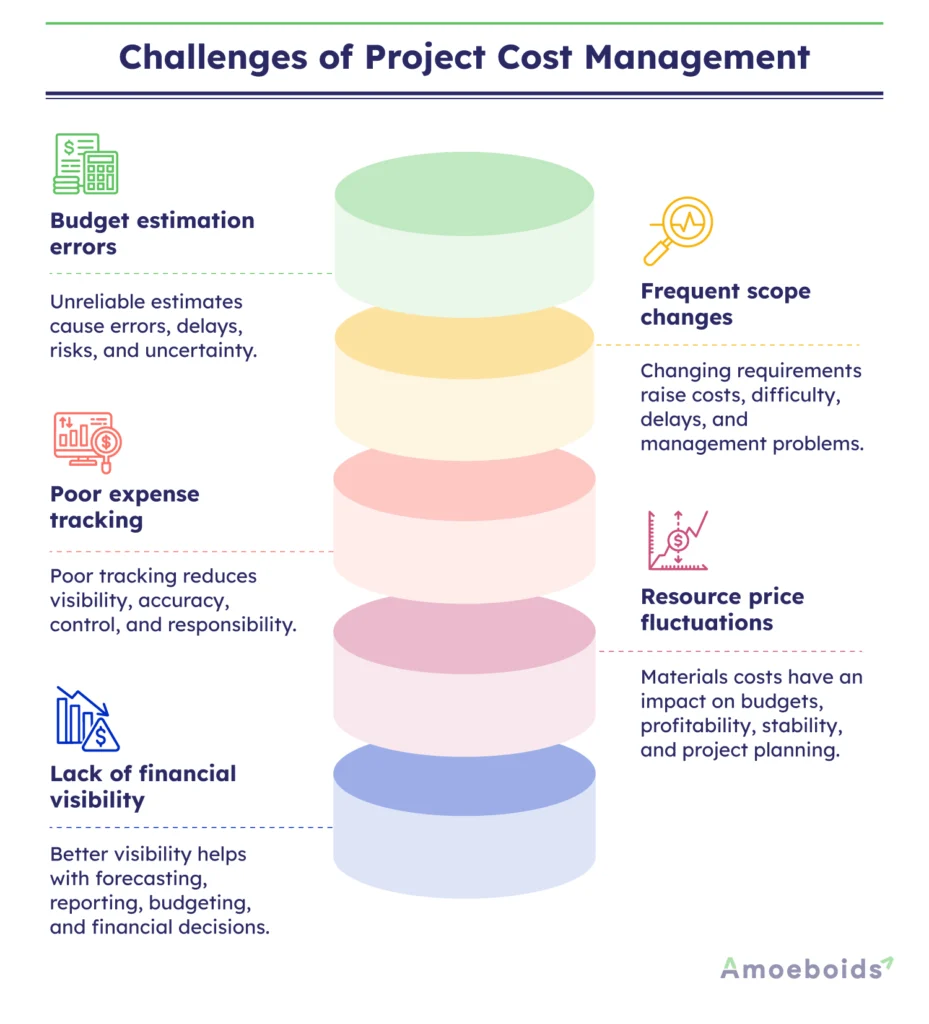

Challenges of Project Cost Management

Budgeting appears simple on paper, but real-world projects frequently involve unexpected costs, changing priorities, and resource constraints. The following are common project cost management challenges that affect budgeting, planning, and financial control.

Budget Estimation Errors

When initial estimates are unrealistic or incomplete, even the best project cost management plan can fail. Minor errors in work, materials, or timelines frequently lead to budget overruns later.

Scope Changes Frequently

One of the most difficult challenges in project cost management processes is dealing with changing project requirements. Additional features, client requests, or design modifications can quickly add to overall project expenses.

Poor Expense Tracking

There is a lack of reliable project cost management software and proper financial monitoring. Teams may struggle to accurately track spending, invoices, and resource costs throughout the project’s lifecycle.

Resource & Material Price Fluctuations

In industries such as construction project cost management, changes in material prices and labor costs can quickly raise project costs. Vendor rate fluctuations can have an impact on both the approved budget and overall profitability.

Lack of Financial Visibility

Using strong project cost management best practices improves forecasting and budget allocation throughout the project lifecycle. It also allows for enhanced cost reporting and more smart choices before financial matters become hard to manage.

Project cost management processes

Project cost management processes provide structure by outlining a clear sequence of steps for planning, tracking, and controlling costs from beginning to end.

1. Cost planning

The foundation is laid at this stage. Teams decide who will be in charge of approvals, what tracking tools will be used, and how project expenses will be managed. Planning also entails identifying financial risks and laying out plans to mitigate them throughout the project.

2. Cost estimating

Once the plan is in place, it’s time to forecast. This involves calculating how much each activity will cost using historical data, vendor quotes, and expert judgment. As noted in RSIS International’s review, modern estimating often combines predictive analytics and real-time data to refine accuracy and reduce human error.

3. Budgeting

Here, all cost estimates are consolidated into a single approved budget that serves as the financial baseline. Teams can monitor performance and identify deviations early with the aid of this baseline. Earned value analysis, for example, can be used to rapidly ascertain whether a project is falling behind schedule or spending more than anticipated.

4. Cost control

This is where planning meets reality. Teams keep a lookout for discrepancies between approved and actual spending and take corrective action as soon as they are discovered. This step is made more effective and less prone to errors by tools that automate reporting and spot patterns of excessive spending.

These four processes aren’t separate checkboxes. They work best when viewed as an ongoing cycle. Each stage leads to the next, ensuring that the project stays financially healthy while maintaining quality and stakeholder confidence.

Project cost estimation example

Let’s examine how these steps are actually carried out through a project cost management example. Consider a mid-sized software company that intends to add a new customer service feature to its existing platform. The group decides on a three-month schedule, divides up the work, and starts projecting costs.

| Cost Element | Estimated Cost ($) |

| Developer Salaries | 50,000 |

| Software Licenses | 5,000 |

| Testing Tools | 3,000 |

| Contingency Reserve | 7,000 |

| Total Budget | 65,000 |

The strategy behind the numbers matters. Developer salaries are direct costs associated with the project’s primary deliverable. Licenses and testing tools are variable expenses that fluctuate depending on scope and usage. The contingency reserve protects the team from unplanned challenges, such as changes in client requirements or delays in integration.

The project manager sets $65,000 as the cost baseline and begins tracking actual spending once work starts. With cost control methods such as Earned Value Management (EVM), managers can compare planned versus actual costs in real-time and make corrections before overruns occur.

When teams combine thoughtful planning with reliable tracking tools, budgets become not just limits but instruments for smarter decision-making.

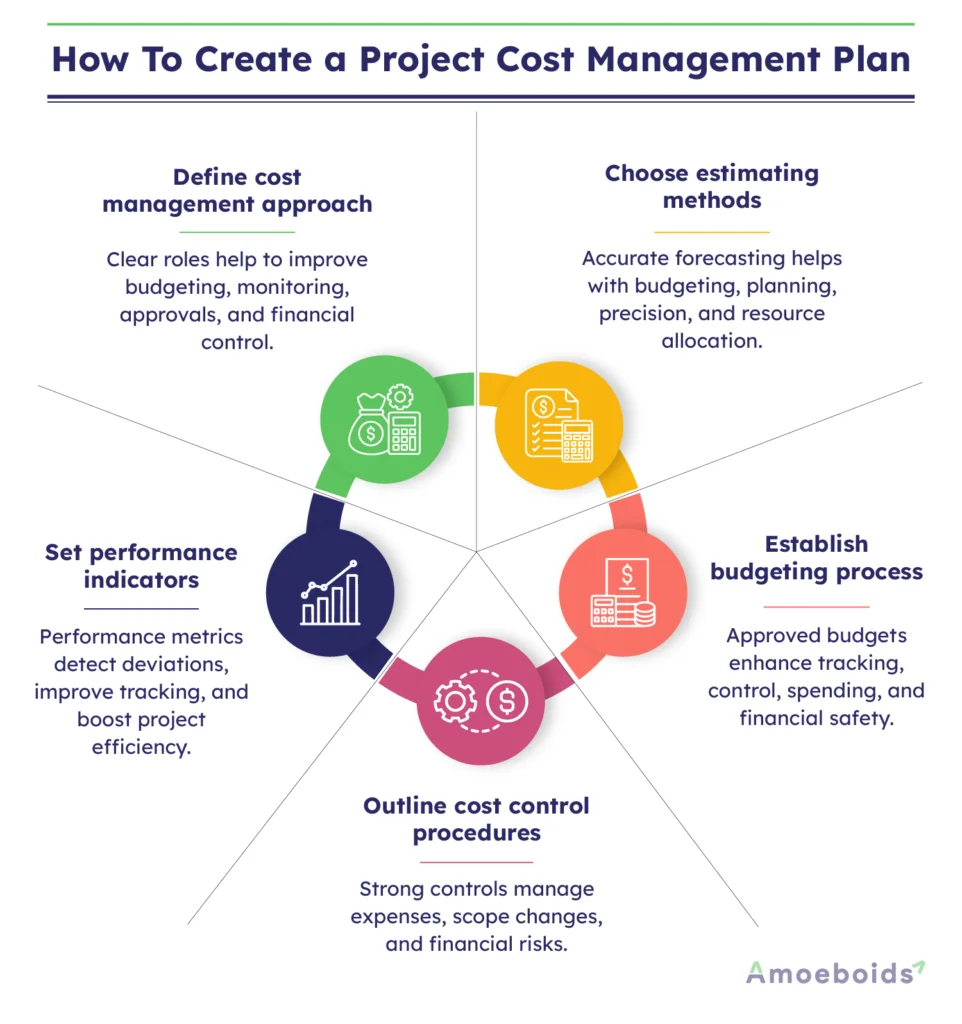

How to create a project cost management plan

A well-designed project cost management plan serves as your roadmap for managing every dollar throughout the project lifecycle. It outlines the who, what, when, and how of financial control, ensuring that no cost decision is left to guesswork.

1. Define the cost management approach

Start by outlining the procedures for managing, monitoring, and approving costs. Roles and responsibilities should be outlined in this section, including who approves spending, who monitors budgets, and how often reports will be examined.

2. Choose the right cost estimating methods

Some teams rely on historical data, while others use expert judgment or parametric models. The goal is to predict costs accurately without inflating the budget. Insights from Aston Research Explorer suggest combining traditional estimation with predictive analytics to improve forecasting precision.

3. Establish the budgeting process

Once the estimates are ready, consolidate them into a single, authorized budget. Comparing actual spend to this baseline helps you detect deviations early and correct them before they escalate.

4. Outline cost control procedures

This step defines how the team will handle unexpected expenses and scope changes. According to RSIS International, projects that maintain consistent documentation and stakeholder communication are more likely to stay within budget and adapt quickly to change.

5. Set up performance measurement indicators

Establish quantifiable metrics like Earned Value (EV), Schedule Variance (SV), and Cost Performance Index (CPI). Serving as early warning signs, these indicators enable you to spot project deviations.

Even the best cost plan can fall short if teams lack visibility. That’s where integrated project management tools come in.

Who is Responsible for Cost Management in a Project?

Successful project cost management is usually a collaborative effort between project managers, finance teams, stakeholders, and department heads. The points listed below explain who manages project costs and how each role contributes to effective budget control.

- Project Managers Lead: The role of the project manager is mainly to manage the project budget, track expenses, forecast and manage the overall project cost management plan throughout the project lifecycle.

- Finance Teams Support: Finance professionals monitor cash flow, approve budgets, process invoices, and ensure that spending meets the company’s financial goals and reporting standards.

- Stakeholders Approve Decisions: Clients, executives, and stakeholders review project budgets, approve additional expenses, and help in organising spending during significant project changes.

- Team Leads Manage Resources: Department heads and team leaders manage employee costs, resource allocation, timelines, and operational costs to avoid unnecessary spending.

- Construction Teams Monitor Costs: In construction project cost management, contractors, procurement, and site managers regularly keep a close watch on the material pricing, personnel costs, and vendor costs.

Project Cost Management Tools & Software

Using the right project cost management tools helps teams track expenses, enhance estimation, and maintain better financial control throughout the project. The points below highlight how software solutions simplify cost planning and budget management.

- Budget Tracking Software: Modern project cost management software helps teams monitor expenses, compare planned versus actual costs, and generate accurate financial reports easily.

- Real-Time Cost Monitoring: Many tools include live dashboards that provide better insight into spending, resource usage, cash flow, and project profitability.

- Automated Reporting Features: Automation streamlines tasks such as invoicing, expense tracking, financial analysis, and stakeholder reporting.

- Better Planning & Forecasting: Advanced platforms allow smarter budgeting, resource planning, risk analysis, and forecasting to ensure future financial security.

- Supports Cost Management Processes: Successful software helps teams manage approvals, track budget changes, and maintain financial quality more effectively, thereby improving overall project cost management processes.

Best practices for project cost management

Consistency, communication, and real-time awareness are essential for efficient project cost management. The following practices help teams in maintaining responsiveness and financial discipline over the course of a project.

Collaborate early and often

Open communication prevents overruns. RSIS International found that proactive stakeholder involvement reduces financial risk and strengthens accountability.

Use a work breakdown structure

Clear task mapping improves estimation accuracy. The Journal of Project Management (GrowingScience, 2024) reports that structured scope control leads to better cost performance.

Apply predictive analytics

Combining historical data with analytical models improves forecasting precision. Aston Research Explorer highlights that data-driven estimation minimizes error and bias.

Track costs in real time

Continuous monitoring enables faster corrections. The RSIS International study found that automated cost tracking yields measurable savings.

Adapt to project context

Each project faces unique financial pressures. Aston Research Explorer emphasizes adjusting cost strategies to match industry and market conditions.

Train teams continuously

Knowledge drives accuracy. Modern software supports skill-building by simplifying forecasts and visualizing spending patterns.

When combined, these techniques help teams transition from reactive cost control to proactive cost leadership.

Using project cost management to your advantage

Fundamentally, project cost management provides teams with the information they need to make informed decisions, the insight they require to act quickly, and a framework for efficient planning. Open communication, continuous learning, and real-time monitoring distinguish projects that consistently meet or exceed expectations from those that don’t.

Amoeboids provides solutions that simplify the daily application of this discipline for teams utilizing Atlassian tools. When these tools work together, managing project costs becomes intuitive. Teams can detect discrepancies promptly, convey them effectively, and sustain progress while staying mindful of the budget.

Discover the complete range of Amoeboids apps to understand how automation and organized cost management can assist your teams.

FAQs

Q1: What is the project cost in project management?

The project cost includes all financial resources necessary to complete project activities, including labor, materials, equipment, and overhead related to the project scope.

Q2: What is the aim of project cost management?

The primary aim is to plan, estimate, budget, and control project costs to complete the project within the approved budget while maximizing value.

Q3: Who is responsible for cost management in a project?

The project manager typically leads cost management, supported by a cost control team and financial experts, ensuring costs are tracked, reported, and controlled effectively.